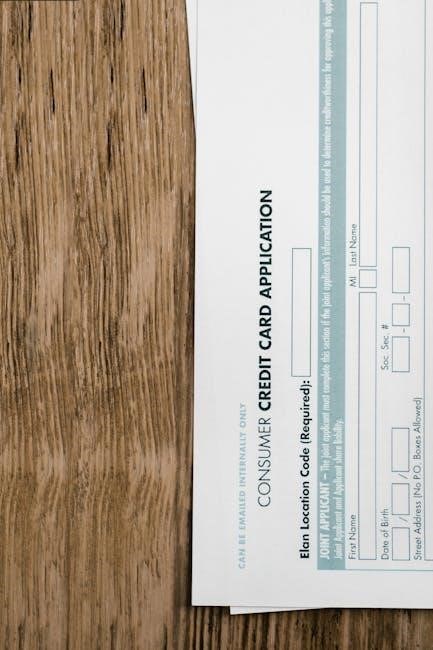

New Customer Credit Application Form PDF: A Comprehensive Guide

New customer credit application forms, often in PDF format, are vital tools for businesses to evaluate creditworthiness, manage risk, and ensure legal compliance.

What is a New Customer Credit Application Form?

A new customer credit application form is a formal request, either oral or written, for extending credit to a new client. Typically, this takes the shape of a standardized document used by businesses to gather essential information. This information is crucial for assessing the applicant’s ability to repay borrowed funds.

These forms, frequently available as a PDF, serve as an authorization for the business to investigate the customer’s credit history. Financial institutions and lenders utilize a fixed Credit Application Template, often a printable business form, to maintain consistency. The completed form affirms the accuracy of the provided details, enabling informed credit decisions and mitigating potential financial risks for the lending entity.

The Importance of Credit Application Forms for Businesses

Credit application forms are essential tools for businesses, enabling informed decision-making and minimizing financial risks when extending credit to new customers. These forms, often distributed as a PDF, facilitate a standardized process for evaluating creditworthiness. They allow businesses to gather vital financial and personal data, including income, expenses, and credit history.

By utilizing a consistent Credit Application Template, companies can efficiently assess risk and determine appropriate credit limits. The form also functions as an authorization, permitting businesses to verify information and conduct necessary credit checks. This diligent approach safeguards against potential losses and fosters responsible lending practices, ultimately contributing to a healthier financial standing for the business.

Key Components of a Standard Credit Application Form

A typical new customer credit application form PDF includes several core elements. Firstly, comprehensive applicant information – personal details for individuals, or legal structure and ownership specifics for businesses – is crucial. Secondly, detailed financial information, encompassing income and expenses, is required for assessing repayment capacity.

Furthermore, a standard form necessitates a credit history disclosure and authorization section, allowing verification of past credit behavior. Bank and trade references are also vital, providing insights into financial stability and business creditworthiness. These components, often found within a Printable Business Credit Application Form, collectively enable lenders to make informed credit decisions.

Essential Sections of the Form

Essential sections of a new customer credit application form PDF include applicant details, business information, and a thorough review of financial history.

Applicant Information: Personal Details

This crucial section of the new customer credit application form PDF gathers fundamental identifying information. Typically, it requests the applicant’s full legal name, current residential address, date of birth, and contact details – including phone number and email address.

Social Security Number (SSN) or Taxpayer Identification Number (TIN) is often required for identity verification and credit reporting purposes. Some forms may also ask for marital status and number of dependents. Accurate personal details are paramount for identity checks and ensuring proper communication throughout the credit process.

Providing complete and truthful information in this section is essential for a smooth and efficient application review.

Business Information (If Applicable): Legal Structure & Ownership

When a new customer credit application form PDF is completed by a business, this section becomes critical. It requires detailed information about the company’s legal structure – whether it’s a sole proprietorship, partnership, LLC, or corporation. The full legal business name and address are essential, alongside the business’s registration number and date of establishment.

Ownership details are also vital, listing all owners, partners, or shareholders with their respective percentage of ownership. This section often requests information about key personnel, such as the CEO or CFO. Understanding the business’s structure and ownership helps lenders assess the overall risk and financial stability of the applicant.

Financial Information: Income and Expenses

The ‘Financial Information’ section of a new customer credit application form PDF is arguably the most scrutinized. Applicants must provide a comprehensive overview of their financial health, including detailed income statements. This typically involves listing all sources of income – salary, profits, investments – and their respective amounts, often requiring supporting documentation like pay stubs or tax returns.

Equally important is a breakdown of monthly expenses, encompassing both personal and business costs. This includes rent/mortgage, utilities, loan payments, and operating expenses. Lenders use this data to calculate debt-to-income ratios, assessing the applicant’s ability to repay the requested credit.

Credit History and References

A new customer credit application form PDF requires detailed credit history disclosure and references to verify financial reliability and past payment behavior.

Credit History Disclosure and Authorization

The new customer credit application form PDF necessitates a clear credit history disclosure section; This empowers businesses to obtain a comprehensive understanding of the applicant’s financial past. Crucially, the form must include a legally sound authorization clause.

This authorization permits the business to access the applicant’s credit report from recognized credit bureaus. It’s essential to specify which bureaus will be contacted and the purpose of the report retrieval – assessing creditworthiness for extending credit.

Applicants must explicitly consent to this access, acknowledging their rights regarding credit reporting. The authorization should also detail how the information will be used and protected, aligning with data privacy regulations. A clear statement regarding the applicant’s right to receive a copy of the credit report is also vital for transparency.

Bank References: Providing Financial Stability Proof

A new customer credit application form PDF frequently requests bank references as a key component of financial stability verification. This section asks applicants to provide details of their primary banking relationship, including the bank’s name, address, and contact information.

The purpose is to allow the business to independently verify the applicant’s account history and overall financial health. Businesses may contact the bank to confirm account balances, transaction patterns, and the length of the relationship.

Applicants typically need to authorize the bank to release this information. Providing accurate and up-to-date bank reference details is crucial for a swift and positive credit assessment. It demonstrates transparency and a willingness to substantiate financial claims, bolstering the application’s credibility.

Trade References: Assessing Business Creditworthiness

Within a new customer credit application form PDF, trade references play a vital role in evaluating a business’s creditworthiness, particularly for business-to-business (B2B) credit applications. This section requires applicants to list suppliers or vendors with whom they have established credit accounts.

Providing contact information – names, addresses, and phone numbers – allows the business extending credit to inquire about the applicant’s payment history and reliability. These references offer insights into how consistently the applicant meets its financial obligations to other businesses.

Strong trade references demonstrate a history of responsible credit management, increasing the likelihood of approval. Accurate and current information is essential for a thorough assessment, showcasing a trustworthy business reputation.

Legal and Compliance Aspects

New customer credit application form PDFs must adhere to regulations like the ECOA and TILA, ensuring fair lending practices and data privacy.

Data Protection and Privacy Policies

New customer credit application form PDFs necessitate robust data protection and privacy policies due to the sensitive personal and financial information collected. Businesses must clearly outline how applicant data will be used, stored, and secured, complying with relevant data protection laws.

Transparency is key; applicants should be informed about their rights regarding their data, including access, correction, and deletion. A comprehensive privacy policy should detail data retention periods and any third-party access. Secure data transmission methods, like encryption, are crucial, alongside adherence to industry best practices for data security. Failing to protect applicant data can lead to legal repercussions and damage a company’s reputation, emphasizing the importance of prioritizing data privacy.

Equal Credit Opportunity Act (ECOA) Compliance

New customer credit application form PDFs must strictly adhere to the Equal Credit Opportunity Act (ECOA). This federal law prohibits discrimination in any aspect of the credit process based on race, color, religion, national origin, sex, marital status, or age.

Forms should avoid requesting information related to these protected characteristics. Any questions asked must be directly related to creditworthiness. Businesses must provide clear adverse action notices if an application is denied, detailing the specific reasons for the denial. Proper ECOA compliance demonstrates a commitment to fair lending practices and avoids potential legal penalties. Thorough staff training on ECOA regulations is essential for ensuring consistent and lawful application processing.

Truth in Lending Act (TILA) Considerations

When designing a new customer credit application form PDF, adherence to the Truth in Lending Act (TILA) is crucial. TILA mandates clear and conspicuous disclosure of credit terms, including the Annual Percentage Rate (APR), finance charges, the amount financed, and the total of payments.

The application should not contain misleading information regarding credit terms. If the application is for an open-end credit plan (like a credit card), specific TILA disclosures are required. Businesses must ensure that all disclosures are easily understandable by applicants. Compliance with TILA fosters transparency and protects consumers from deceptive lending practices, building trust and avoiding legal repercussions.

Form Format and Accessibility

New customer credit application form PDFs offer convenience, but online forms provide enhanced accessibility and streamlined data collection for businesses.

PDF Format: Advantages and Disadvantages

Utilizing a new customer credit application form in PDF format presents both benefits and drawbacks for businesses and applicants. Advantages include universal readability across different devices and operating systems, ensuring consistent formatting regardless of the user’s software. PDFs also facilitate easy distribution via email and website downloads, and can be secured with password protection to safeguard sensitive financial information.

However, PDFs can be less user-friendly for completion, particularly on mobile devices, requiring specialized software for editing. Data extraction from completed PDF forms can be cumbersome and often necessitates manual entry, increasing processing time and potential for errors. Accessibility can also be a concern if the PDF isn’t properly tagged for screen readers, potentially excluding users with disabilities. Online forms generally offer a more interactive and accessible experience.

Online vs. Paper Application Forms

When considering a new customer credit application form, businesses must weigh the pros and cons of online versus traditional paper-based methods. Paper forms, while familiar, are prone to errors, loss, and require manual data entry, slowing processing times. They also present higher storage costs and environmental impact.

Online forms, conversely, offer instant data capture, automated validation, and streamlined workflows. They reduce errors, accelerate approvals, and provide a better customer experience. Digital forms integrate seamlessly with CRM and credit scoring systems, enhancing efficiency. However, online forms require robust security measures to protect sensitive data and may exclude customers lacking internet access. The choice depends on business needs and target audience.

Ensuring Form Accessibility for All Users

A crucial aspect of a new customer credit application form, particularly in PDF format, is accessibility. Forms should comply with accessibility standards like WCAG to accommodate users with disabilities. This includes providing alternative text for images, ensuring proper form field labeling, and keyboard navigability.

Best Practices for Form Design

Effective new customer credit application form design prioritizes clarity, logical flow, and secure data handling for a positive applicant experience.

Clear and Concise Language

Employing plain language is paramount when crafting a new customer credit application form PDF. Avoid industry jargon, complex legal terms, and ambiguous phrasing that could confuse applicants. Each question should be straightforward and easily understood by individuals with varying financial literacy levels.

Conciseness is equally crucial; keep questions brief and to the point. Lengthy paragraphs or convoluted sentence structures can deter completion and increase the risk of errors. Use active voice and avoid double negatives. The goal is to facilitate a smooth and efficient application process, encouraging honest and accurate responses. A well-written form minimizes misunderstandings and potential disputes, ultimately benefiting both the business and the applicant.

Logical Form Flow and Organization

A well-structured new customer credit application form PDF should guide applicants through a logical progression of questions. Group related inquiries together, creating distinct sections for personal information, business details (if applicable), financial history, and references.

Begin with basic identifying information before delving into more sensitive financial data. Employ clear headings and subheadings to delineate each section. Consider using a numbered or bulleted list format for questions within each section to enhance readability. A logical flow minimizes applicant frustration and ensures all necessary information is collected in a coherent manner. This organization also streamlines the internal review process for credit analysts.

Secure Data Transmission and Storage

Given the sensitive financial information contained within a new customer credit application form PDF, robust security measures are paramount. When utilizing online forms, employ HTTPS encryption to protect data during transmission. For PDF submissions, ensure secure file transfer protocols are in place.

Upon receipt, store completed applications on secure servers with restricted access controls. Implement data encryption at rest to safeguard against unauthorized access. Regularly back up data to prevent loss and maintain data integrity. Compliance with data protection regulations, like GDPR or CCPA, is crucial. Prioritize security to build trust and protect both your business and your applicants.

Post-Application Process

Following submission of the new customer credit application form PDF, a thorough credit analysis is conducted, leading to a decision and subsequent notification.

Credit Analysis and Decision-Making

Upon receiving a completed new customer credit application form PDF, businesses initiate a detailed credit analysis process. This involves verifying the information provided, assessing credit history through reports, and evaluating the applicant’s financial stability.

Key factors considered include income, expenses, existing debts, and payment history; Trade and bank references are also scrutinized to gauge business creditworthiness. The analysis aims to determine the applicant’s ability to repay borrowed funds responsibly.

Based on this comprehensive evaluation, a credit decision is made – approval, denial, or conditional approval with adjusted credit limits or terms. A robust analysis minimizes financial risks and supports informed lending practices.

Notification of Application Outcome

Following thorough credit analysis of the submitted new customer credit application form PDF, applicants must receive timely notification of the decision; This communication should clearly state whether the application was approved, denied, or conditionally approved.

If approved, the notification should detail the credit limit, interest rate, repayment terms, and any associated fees. A denial requires a clear explanation, referencing the specific reasons based on credit report findings or application inaccuracies.

Providing this transparency fosters trust and complies with regulations like the Equal Credit Opportunity Act. Prompt and informative notifications enhance customer experience, even in cases of adverse decisions, maintaining a professional relationship.